Lance Stals: Good afternoon everyone. My name’s Lance Stals. I’m a senior solutions manager here at Medallia. I have been in this space almost 15 years with over a third of that coming from omnichannel and conversational intelligence, and I’m really excited. To be here today to walk you through how we trace the real reason behind a call.

So how I’m gonna frame this up, we’re gonna start by discussing the digital experience blind spot. This really isn’t a digital specific session as the title of it may infer, but it does speak best to really how data can live in silos. How we easily can miss the most impactful opportunities that we have as CX leaders.

We’ll discuss what this looks like from the perspective of the customer, how badly a broken experience can really impact things like loyalty, trust. Future sales share of wallet. And then I’m gonna show you how we can actually understand root cause when we’re harmonizing customer [00:01:00] experience from multiple signals and how that derives meaningful, actionable insights.

And then we’ll end where you can start. If this story feels familiar to you,

let’s think about how we act as consumers. And I might ask for a little bit of audience participation when you go to your favorite retailer. You go to your utility provider’s website, your banking app, your healthcare provider website, you can accomplish what you set out to do whatever that task was.

The idea here is customers don’t report friction when it’s happening. We are an innately selfish species in the moment. I’m not gonna tell you. In a survey that I couldn’t complete my task. I’m gonna look for all the pathways that folks like you and others in your organization have laid out for me to do what I came to do.

I’m trying to accomplish a task. I’m not in those spaces to tell you how great or how bad of a job that you [00:02:00] did. So right off the bat, I’m exempt from that solicited feedback loop. If eventually you do get to me. At a point in my life where I feel like I have time and I’m willing to give you feedback, that signal is broken, it’s delayed, and there’s potentially thousands of other customers that have experienced the same exact struggle, is potentially resulting in millions of dollars and lost revenue or increased operational costs.

As we’re engaging with that support center and what the customer is calling for gets manually reported by the agent. We’re accounting for what may be representative of the call reason, but it’s not representative of

why the customer is calling. Despite that the problem is visible, but only within that conversation itself.

Now you might say, Lance, I can get this information from my survey data. And I like the solutions engineer that I will always be at heart. [00:03:00] I might say, yeah, maybe. But did you know that Forrester research shows that about half of firms fail to reach a 10% survey response rate? Did you know three fourths struggle to attain 20% response rate across all channels?

My question to you would be, why would you leave 80 to 90% to chance in Vegas at home, on my couch in metro Detroit, on FanDuel? We’d say those are pretty bad odds. So the problem’s right in front of us, we just can’t see it. The point is, surveys alone, they cannot diagnose all the digital friction. Digital failures, they’re gonna show up as interactions in your contact center.

And without connecting to those signals, we’re blind to root cause and ROI opportunities. Marrying that survey data to conversational data and behavioral data is really what will reveal the full picture [00:04:00] of why, what. Where behind every single issue that comes up in those interactions. So how do we use our contact center data to understand that real reason behind a phone call?

Not the task the customer has, but why they had to call for that to complete that task at all. Our problem is in that spaceship. We just haven’t noticed it yet.

Meet Russell. Russell is usually starting his day off, mildly annoyed, but today something particularly unusual happens when he logs into his online banking app.

Russell spots some transactions that he’s not familiar with. I think all of us are probably pretty familiar with that sinking feeling, looking at your checking account. It’s an electronic store in Moscow, a couple of casino transactions and a place. He is nowhere near $1,400. Gone just missing from his account.

Russell clicks into those transactions. He [00:05:00] expects to be able to report those transactions and dispute it as fraudulent. Unfortunately, he’s hit a dead end and he cannot act on this. So Russell goes back to his account page. He remembers there’s a live chat function on the homepage of the account managing the banking app.

He’s super stressed as anyone would be. When $1,400 just randomly goes missing, and he is, hoping to get some help. He opens up the chat. He’s met by a lovely chatbot who after some time and frustrating back and forth, escalates to a live agent. Chatbot can’t help him. So Russell finally reaches that human being and they can’t help him either.

He’s basically told you need to call in. So at this point, he is on his third attempt. To dispute these transactions, digital failed him. The chat bot failed him. The live chat agent failed him. So on his fourth attempt, Russell finally gets the help he needs. The agent he speaks to is [00:06:00] lovely. She’s helpful, she gets the transactions flags.

He follows all the appropriate steps and regulatory processes. However, during this call, Russell voices his frustration with the mobile app. He describes the issues that he had with the chat bot, and he didn’t love the fact that he actually had to call into the contact center. So everything that we need to know about this experience end to end is it within that phone call.

But it sits in isolation in the contact center where it’s really only used to give Nicole our agent props for how well she handled an extremely frustrated Russell. And that’s good for Russell, right?

Here’s the problem. Russell is one of thousands of Diamond Bank customers who are experiencing that issue.

This happens every single day. They have no way to serve, self-serve, disputing, fraudulent transactions. Several of the support functions in place either don’t know how to help or they’re not [00:07:00] going to help. For whatever reason. So customer effort goes up, frustration goes up, and this leads to Diamond Bank, essentially beginning to lose customers and revenue requires customers call into the support center, increases our costs, doing nothing is basically lose, lose all the way around.

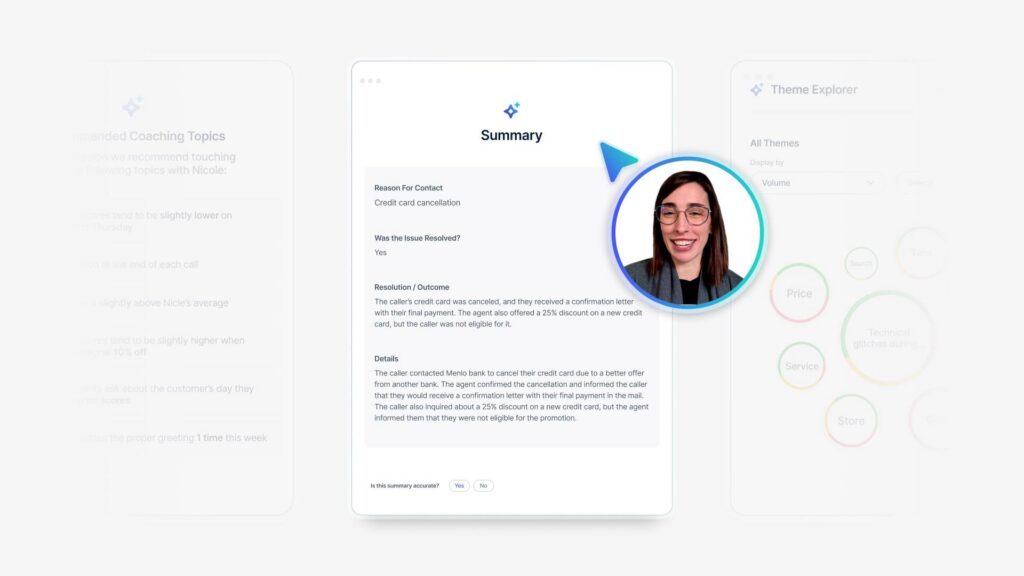

There are several other things that are happening on the backend that we tend not to think about. Number one, all of our calls are being manually tagged by contacts and our agents, and that’s great, but they have a limited menu of contact reasons that they can select from. We ultimately end up with 25% of our calls in a other bucket, and this call is tagged by the agent as a transaction dispute call.

There’s no other context. She can’t give any other context. Was this a call for fraud? It was Russell’s task, but it’s not why he called. Russell does end up completing a survey, but it’s the [00:08:00] post-contact survey that is sent after interacting with Nicole, our agent, and he gives a

low CSAT for the overall experience, but he doesn’t explain why he gave the low score.

He basically just says, yeah, agent was polite, but the experience overall was terrible, so I’m giving you a one out of 10. No context done. Third, our digital behavioral data in this situation looks pretty normal. It just looks like he went to a check. His account balance clicked into a transaction. Then he started to interact with the chat.

There’s no real visible behavioral frustration, right? There’s no way to connect the disparate data point of the behavior to the conversation or the feedback that he’s provided. So the problem exists, right? We just lived it. Yet no single system can seem to see it end to end. We know the spaceship exists, but what’s the solution?

When I was a little kid, I wanted to be Will Smith. [00:09:00] So bad. And now that I’m almost 40, I want to be Jeff Gold bloom so bad. And this is like the coolest thing ever. Yeah. To solve for the problem, right? We have to account for that whole picture to achieve impactful insights and actions. So unifying those siloed data streams across survey.

Across behavior, across conversational intelligence as like the mothership to the insight is really gonna harmonize those data sets that exist, but currently are heavily siloed, mitigating that ability to understand the true impact of our problem. We can do this. Let me show you how. So we have another single interaction just like Russell.

This one, the guy’s named Deroy know if you’ve heard of him, Roy Kent. And Roy is at risk for churn. We’re picking up this [00:10:00] one out of 10 and his CSAT score and post-contact survey, and it’s pretty similar to the experience that RU that we went through with. Russell gives that one out of 10, but we look at his open end and he says, yeah, the agent was polite.

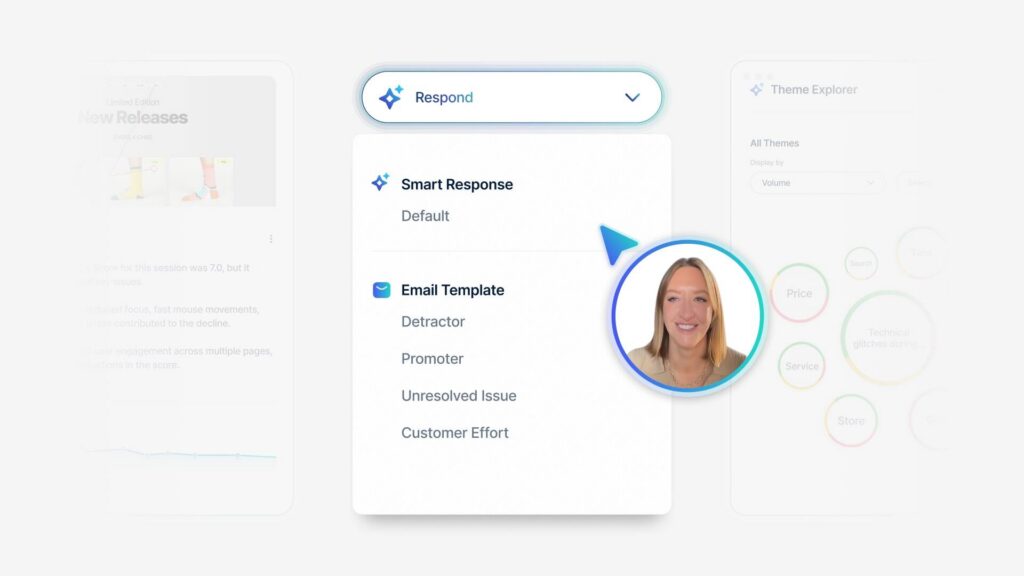

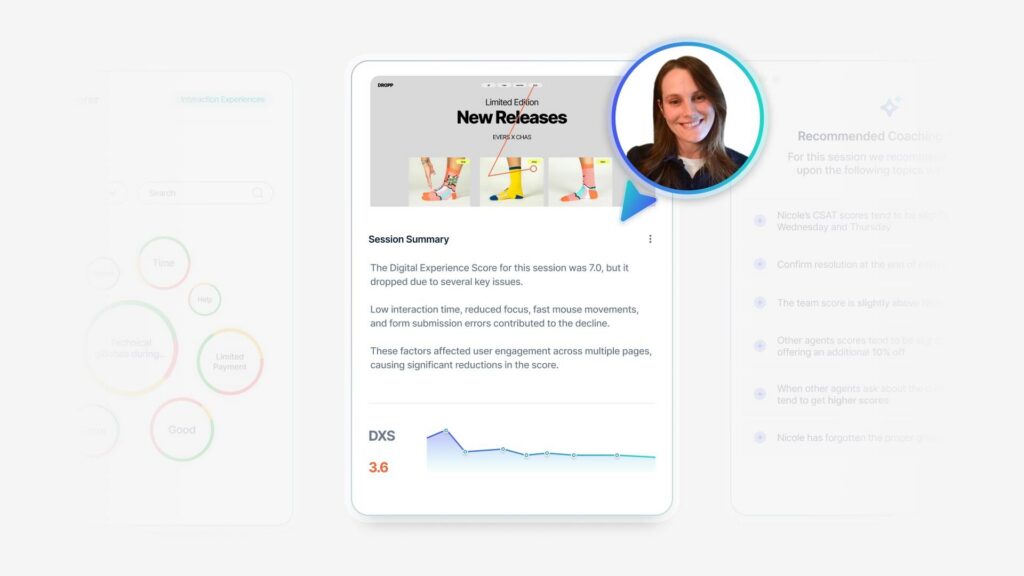

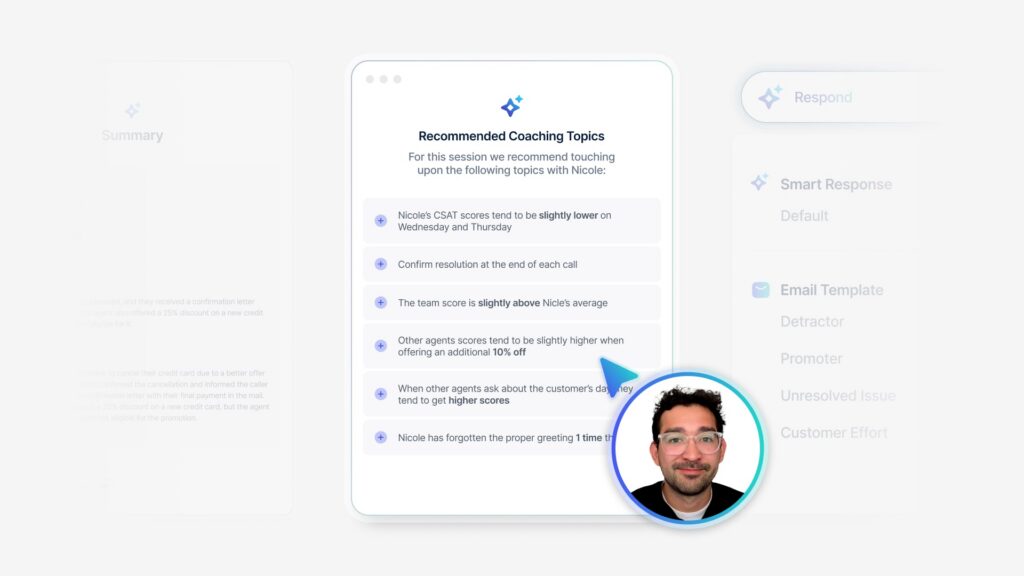

That’s it. Lucky for us. We’re bringing his chat interaction in as well, so we can see why he called. We can see what the resolution was and we can very quickly gain an understanding into the details of this call. We also have what I like to call the DNA of the call visualized within this interaction.

And then we have the transaction itself, and on our left side here, we have all of these different topics that are being tagged within the interaction. Within here. Off the rip, we see, hey, Roy wants to dispute a credit card charge. Great. We get further into the conversation. He says, Hey, I’m pretty [00:11:00] upset.

This is wasting my time. Chatbot can’t help me. All right. Now he’s talking to Nicole, right? Nicole’s getting a lot of these interactions and he makes a suggestion at the end and Nicole does help him via chat, but. Hey, you should make this easier to do on the app or the website, so I don’t need to waste my time with your useless chat bot.

So there’s a couple of things

right at the micro level. We can immediately start actioning this right at the end, at the interaction level inner loop. I can go up here, I can hit comment, I can tag my digital leader. Who’s gonna look into potential feature ads for disputing transactions from a self-service perspective?

I’m gonna get that over to my usability team, who’s responsible for building the prompts in my chat bot and the playbook. In my chat bot to make sure that my chat bot can actually handle these workflows moving forward because it is, in this scenario, it’s a transaction under hun under $200. That’s not gonna [00:12:00] engage like any regulatory issues or anything like that.

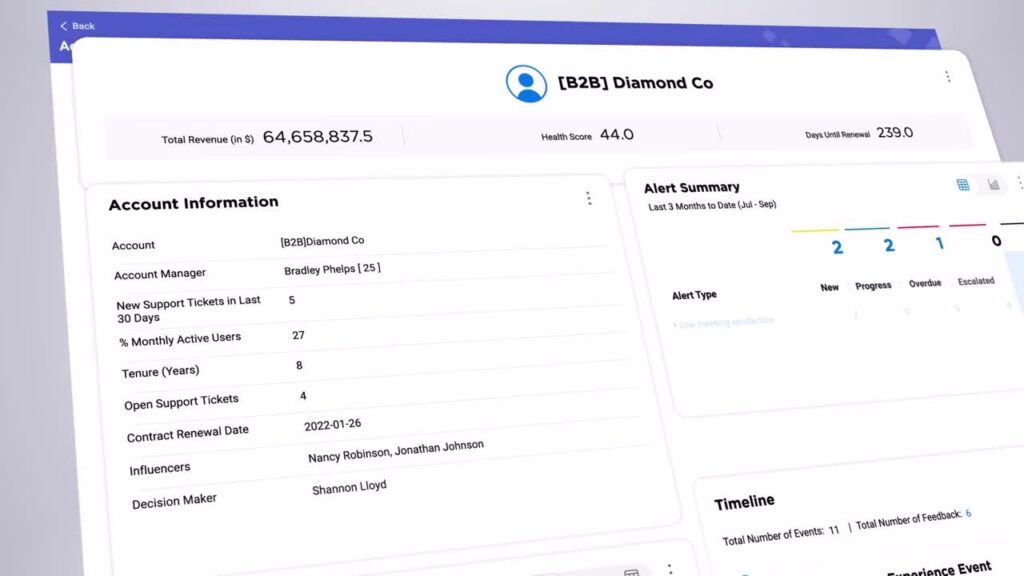

So that’s, at the micro being able to act off of. Roy from the inter loop perspective, outer loop, we actually can respond directly to Roy within his customer profile information. We have his email address. We can reach out to him. We can say, Hey, we’re really sorry that, you had this frustration.

We’ve engaged with our mobile app teams to make this easier moving forward. We’ll keep you posted on it

right now once we scale this out to all of our interactions. The very first thing that we need to understand is what are all the sources that we’re bringing in? In that last one, just for Roy alone, we saw a survey response.

We saw our chat transcript, right? So in omnichannel we’re bringing in all of these different sources. We have calls, we have chats, we have surveys, we have even have our employee notes. It’s agent call notes, right? [00:13:00] One specific thing I wanna call out is. When we’re just looking at surveys, we think our number one issue is logging in and logging out.

It’s a tale as old as time. I think I’ve seen login issues as like a top reason for friction in digital my entire career. But then we look at our chats, credit card disputes. Fraudulent resolution is our number one topic, and we have way more chats in aggregate than we do surveys. So once we have that foundational understanding of what’s in all of this data and we’re taking that text analytics led approach to marry it all together, then we can start layering different lenses over the top of it.

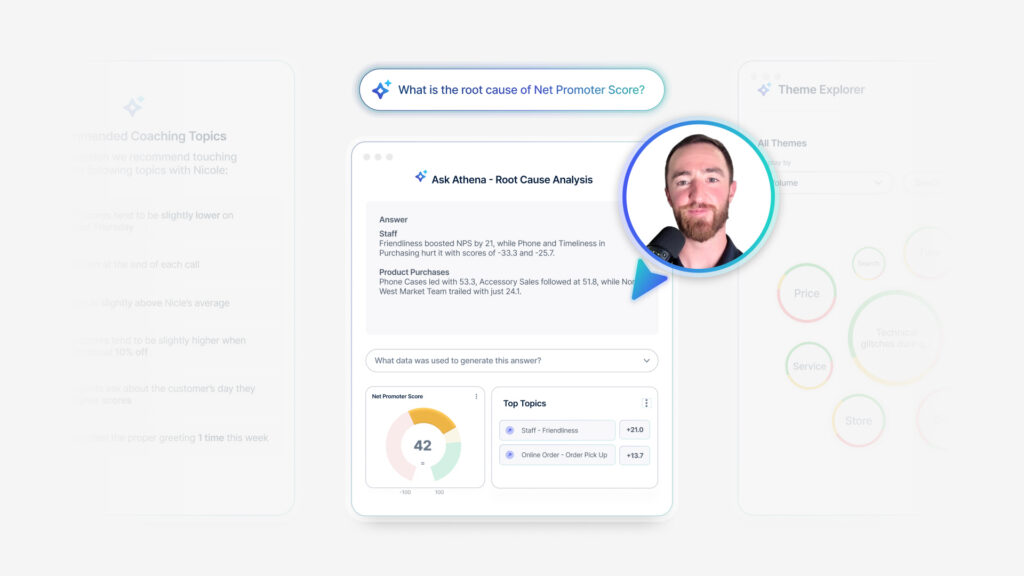

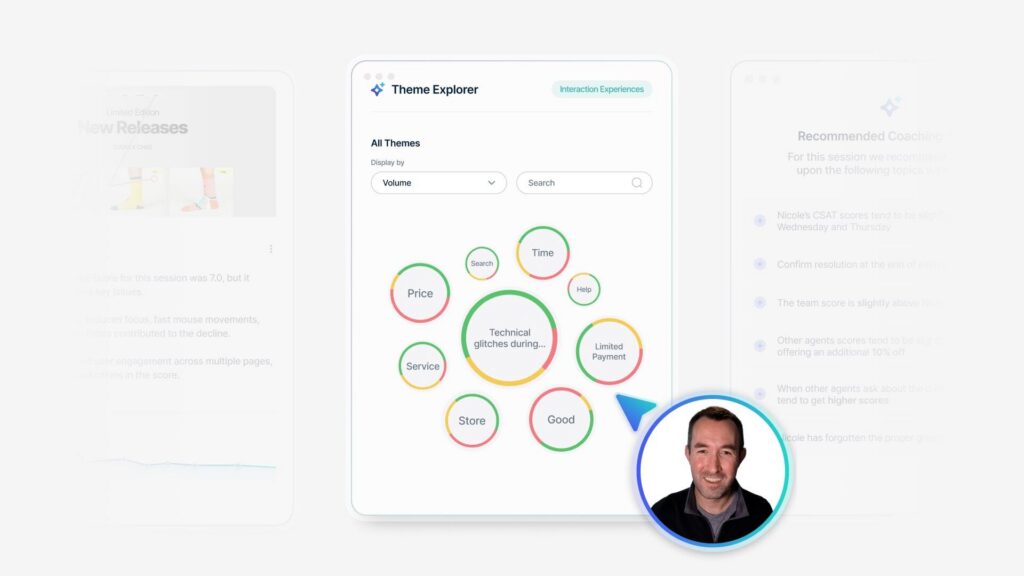

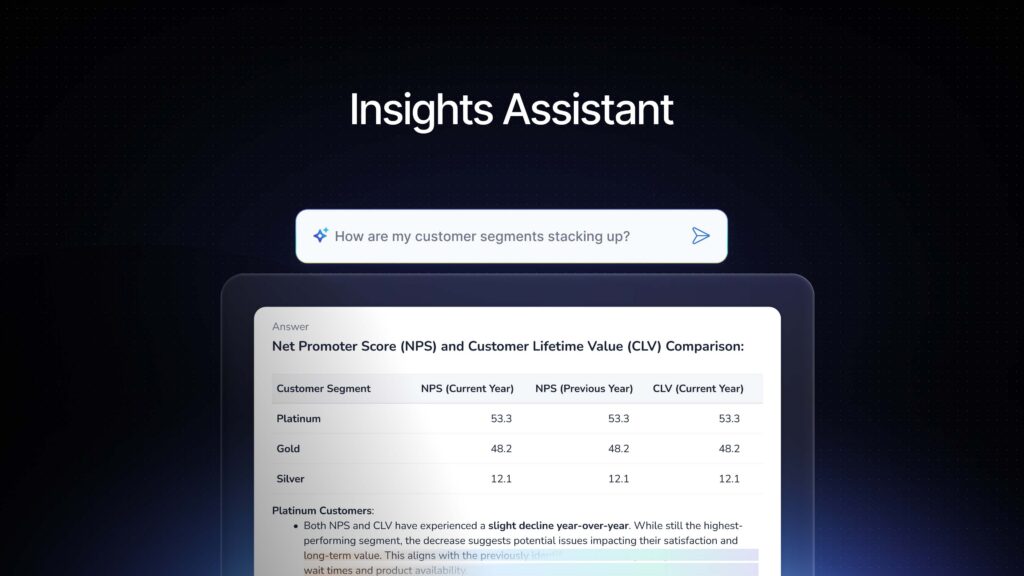

So for example, this is an omnichannel report and I as a CX leader. Aggregate across all of my channels can understand what’s driving customer frustration. [00:14:00] So I have am quantifying frustration in all of these records. And then I have a very quick summary of exactly what’s driving that frustration.

Beyond that, I can see the emerging topics that are driving that frustration. Overall, credit card dispute is number two. Across the entire data set that we’re ingesting. I can dig a little bit further. I can look at some of the themes, I can look at some of the topics, and I can use generative AI to really understand that specific contact reason.

And within this one, I see resolution through the mobile app appears to be lacking or basically non-existent based on, the numerous reports that we’re getting from customers. They experience those problems, they struggle with them. And several customers are also experiencing difficulties and getting new debit cards after they’ve been victims of fraud too.

So that’s almost like our sort of our sub insight [00:15:00] that we’re getting from this. So then the question becomes how do we get this into the hands of the people that can make change, right? And the people who can recognize it and understand its importance. And there’s really two different roles.

There’s the folks in the contact center. That would need to understand how this is impacting them operationally. And then there’s our pals and digital who are actually gonna go and act on the feedback that they’re getting and make improvements to that overall experience. So the first one is our contact center, where we have a contact deflection dashboard where we are identifying and quantifying our self-service failures.

We’re literally looking for people saying, I can’t do this. I want you to help me with, I tried to do this online, I want to do this myself, and can’t. And we’re actually attaching a dollar value to this. And in eight business days, the current month, it accounts for $25,000 in incurred [00:16:00] costs, right? Nearly, or 13% on the nose of my total.

Call volume chat volume is directly tied to self-service failure. What’s driving that self-service failure? In the chats, if we get to see it, there is is those fraudulent transactions. Now, it’s great that I can see that, I can understand it’s volume, I can understand how it’s impacting things like average handle time and cost to serve.

But I wanna know a little bit more about this. So from a contact center standpoint, and our digital teams will have a similar flavor of this, but I can actually deep dive into this topic, right? I have that same topic summary that I saw on the previous dashboard where we had that frustration layer over the top of it.

I can see how this is impacting both operational metrics and CX metrics. And then I can start to understand a little bit more context about it because we’re doing that multi topic tagging across the [00:17:00] entire interaction. And what we find is that Russell and Roy are having issues that a lot of other people are having.

People are complaining about missing features in the mobile app, issues with credit card issues with fraud and resolution related to those disputes. So this is a big issue that, we need to get. We can get the ball rolling on some self-service opportunities for it. So where do we go from there?

This is where we go to an omni-channel view for our digital teams, where we’re truly blending the behavioral data, the solicited feedback that we get from our digital surveys. We’re blending the context and our data, and I can see. How we’re performing from that behavioral standpoint, how that relates to my CSAT scores in digital, and then tie that to self-service resolution and volume in the contact center.

What I like about this chart [00:18:00] is that there was a time when self-service resolution was not great. Our call volume was very high, but as it trends out, we’re actually doing a much better job. We’re not perfect, but we’re on the right track. I can understand why, where users aren’t able to self-service online.

I can tie text analytics topics to specific pages and specific sections of my website that we’re gonna be representative. Those call interactions and I can attach dollar value to it, I can drill into them, and the same can be done with our digital related contact reason, topics in the top, in the contact center.

Again, I see that dispute fraud resolution as the big one. Now, here is where that behavioral data comes into play. Remember with Russell I said it really just looked like a standard account checking account visit. There wasn’t any bird nesting. There was no like rage [00:19:00] clicking or anything like that.

But our usability team still needs to have an understanding of the people who are complaining about this, like where are they going and what is their expectation for where that functionality should live so that it’s intuitive. I drill into that topic now. I have a list of session replays where that was our intent.

I can go and see what those mobile app visits look like with those session replay links if I have done my job today. You’re probably wondering, oh my God, where do I start?

I would say start with the data that you already have access to red tape, internal politics, perceived security risk, are all things that can be blockers.

So start with the data that you can get to really expand that aperture of the data that you have access to, and obviously lean on us, right? To help you get that data. That might be a little bit harder to obtain. [00:20:00] Within your organization. Second, prioritize the data that’s easiest to bring together. That’s gonna be different, from organization to organization.

Sometimes when we think about going omnichannel, like some of the easiest things to get at are like app reviews in this scenario. If you can’t get call transcripts, you can’t get chat transcripts, maybe you can get access to agent notes. Anything that we can do to just make this a more complete picture to understand what’s going on.

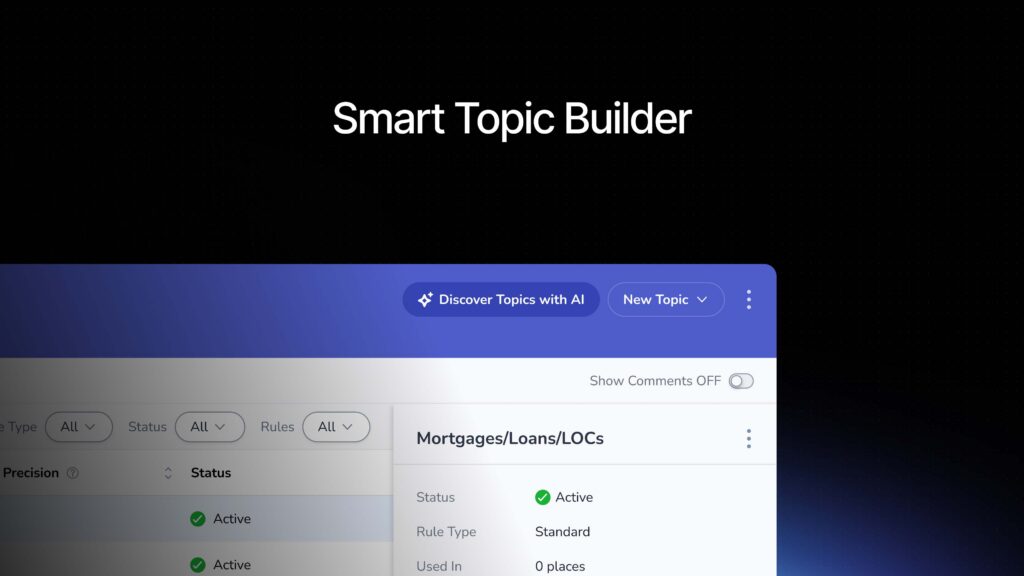

Third. Text analytics lend approach to understanding the data. More explicitly stated, stop score chasing use intent-based topics that are gonna be relative to your business as that primary or foundational layer to understanding what’s going on in all of these unstructured signals. And then use wide net journey specific based topics as your secondary.

From there, that’s when you start to layer on sort of supplemental topic sets, like product type. Quality complaints, [00:21:00] emotion even like risk topics are those different lenses that you can put over the top. Once those patterns are clear in why customers are interacting with you, that’s when we can layer those use case lenses based on those business problems that you’re trying to solve for.

And if I were to put a fifth bullet on this slide, always think about this from. A solutions standpoint. Don’t just build a dashboard to have a dashboard. Make it answer a question that you have. Here’s hoping you leave with your perspective, sharpened confidence strengthened and ready to take what you learn this week and put it into practice.

Thanks everyone so much.